What to know about Chicago's new Development Bond

Because when we're issuing $1.25b in new debt, it's worth understanding why

In April, Chicago City Council passed one of Mayor Johnson’s biggest policy proposals to date, a $1.25 billion Housing and Economic Development Bond that aims to overhaul how the city handles development policy in Chicago. It’s a really big deal. Today I’ll be diving into exactly what the plan entails and why I think it’s a net positive for the city.

As a brief aside off the bat: in earlier posts, I’ve conveyed pretty clearly that I don’t think very highly of the level of managerial competence our current administration has. That remains the case, but it’s not what I’m focused on here today. I think it’s really easy in the context of day-to-day political stuff to lose sight on what ideas are actually good in and of themselves, and that’s bad. With that in mind, I’m focusing here on the merits of the proposal and what bits I think are sound policy, rather than on whether I think the administration is likely to screw things up on the execution side.

With that understood - while I’ve seen some pushback from people I respect, I like this plan. I think it’s a good idea which moves us away from some of the bad parts of city development today, adds flexibility and transparency to development budget, and is largely a pro-growth development for the city of Chicago. It’s not perfect, but I think it’s a big step in the right direction.

Compared to what? (or, How TIFs Work)

If we’re going to talk about how this plan changes city’s approach to development and housing finance, then we need to start with how the city approaches these issues today. That means talking about Tax Increment Financing, or TIF.

TIF districts are a financing tool employed by many municipalities since the 1950s to encourage economic development in specific geographic areas within a given municipality. At a high level, the basic way they work is:

Freeze the assessed property tax base within a given area for 20-30 years. That frozen tax base is what’s available for most government entities (city, county, school district, etc) to tax

When property values go up, whatever incremental tax revenue is collected on the increased value (relative to that frozen assessed base) are set aside and earmarked for the TIF District’s fund

These funds are then used for funding development projects in that neighborhood

To my knowledge, no city uses TIFs more heavily than Chicago. A 2017 report from the Lincoln Institute showed that Chicago has as many TIF districts as the other nine largest cities in the United States combined. We’ve talked about them before - roughly one-third of the city is located within a TIF district. It’s a pretty crazy map:

In total, TIFs account for around 16% of total property taxes collected in the city of Chicago, or $1.3 billion in 2022. I mentioned this before, but please note that doesn’t mean that other entities are forfeiting 16% of revenues they’d otherwise be receiving - instead, it means that your property taxes are higher than they otherwise would be1 to make up for the revenue being diverted into these TIF funds.

I am not a fan of the TIF system. For one, because TIF funds come from the increase in property values, it benefits neighborhoods that are already seeing growth more than neighborhoods which remain blighted. If Fulton Market’s property values double, then the TIF district there2 is flush with cash to reinvest in an already booming neighborhood. Meanwhile, if property values in Englewood remain flat, their TIF remains empty. That seems exactly backwards to me - you’d want to deploy more public resources in the neighborhood that’s currently lacking private investment, not the other way around. TIF districts also last a really long time, with a 23 year lifespan in Chicago3. That’s a really long timeframe for the city to commit itself to developing one neighborhood in particular.

Additionally, I think it needlessly complicates our approach to development. Instead of having one big fund of revenues which we can devote to the best projects across the city, here we have 121 different funds, each of which can only spend money in a specific location. That strikes me as incredibly inefficient, and it’s hard not to think that a lot of those dollars are going to projects that are likely suboptimal at a city level. I’ve written before about how I think it’s stupid to allocate specific tax dollars to specific purposes, instead of putting everything into one fund which we can then allocate appropriately - this is another example of that.

What’s the new plan?

Important backdrop: in the next four years, 45 of those 121 TIF districts (representing about $300mm in annual TIF revenue) are expiring. That means two things; first, our non-TIF property tax base is about to get a fair amount bigger, and second, we’re about to see a significant reduction in dollars devoted towards development unless the city either renews those districts or does something else. I think it’s a good idea for us to do something else.

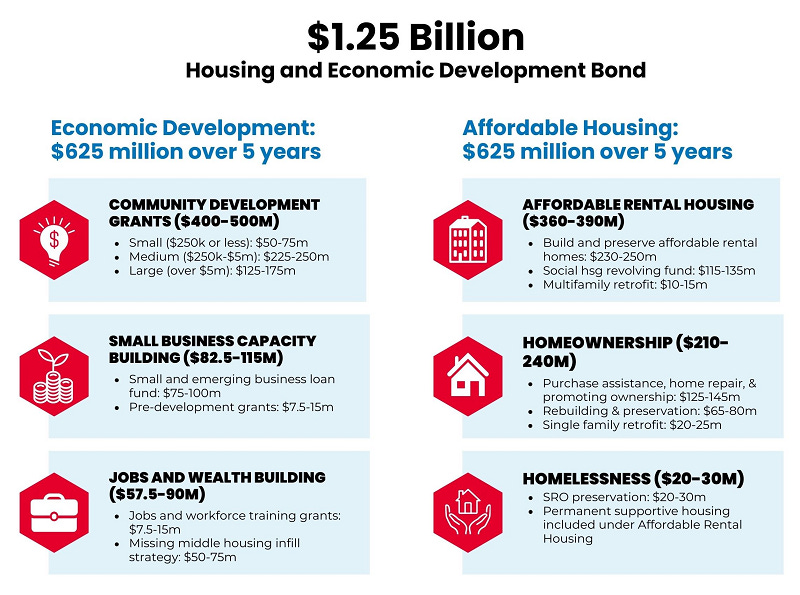

The new plan is intended to be that something else, and reduce our reliance on TIF revenue to fund housing and development projects. The core of the plan is a $1.25 billion municipal bond issuance by the city, with $625 million in revenues going to each of the Departments of Housing (DOH) and Planning & Development (DPD). DOH and DPD would then have a combined $250 million to deploy annually from 2024-2028 on redevelopment projects across the city.

If the bond is how we pay for the spending, how do we pay for the bond? From winding down those TIF districts (not just those 45 coming soon, but all of the others as they expire, too). As the TIF districts close, the city’s property tax base grows - and that growth is more than sufficient to pay off the bond in its entirety and then some. Here’s the projection from the city’s bond book:

I don’t have the city’s estimated amortization schedule on the bond, but $81 million in annual debt service equates to a 30 year repayment term at a 5% interest rate, which seems pretty reasonable given that the bonds issued would be a combination of Chicago’s general obligation (BBB+ rated) and Sales Tax Securitization Corp (AA- rated) bonds. Meanwhile, the city’s revenue from the increased tax base ramps up from ~$50 million per year through 2030 up to over $250 million by the mid 2030s.

I think it’s entirely reasonable to have concerns about any increases to the city’s debt burden - I share those concerns! - but this strikes me as a net positive. If you increase revenue by more than you increase debt service (and if you don’t have to raise property taxes to do so), that’s a good thing.

Another important note from the city’s bond book that I agree with: this better aligns us with best practices across other big cities in the U.S. as well. As I mentioned earlier, Chicago is basically alone in relying on TIFs to fund development - most other cities4 rely on bond issuances to fund housing and development projects. I think that switch is a pretty logical one. Under our current regime, the city often approves bonds on a project-specific basis (they just did this in late May for two TIF projects in the Loop), and then uses TIF funds to cover the debt service on those bonds. This is just cutting out the middle man, and issuing a broader bond which can be deployed for the same purpose without the inflexibility the TIF system requires.

I also think it’s worth noting that Urban Environmentalists Illinois, which I think is the biggest YIMBY group in Chicago, endorsed the plan - you can read their letter in support of the plan here, which highlights a few specific portions of the spending plan as particularly good for housing abundance.

How does this impact our long-term fiscal outlook?

This is really the crux of the issue to me. Obviously the headline here is that we’re adding $1.25 billion to the city’s debt, but I view that as the beginning, not the end, of the conversation here.

For starters, there’s a big difference between incurring debt for nonproductive reasons - like, say, to subsidize construction for an NFL team’s shiny new lakefront stadium - and incurring debt to fund development projects which generate real economic growth in the city. Growth is good, and financing projects to spur that growth can actually help our fiscal position in the long run. I’ve really tried to hammer home in my writing the need for us to foster growth at the city level to deal with our fiscal challenges, and I think this plan is consistent with that idea. Doing things that are growth positive for the city is good, even if doing so incurs (a reasonable, affordable level of) debt along the way.

There’s also a positive fiscal impact to other government entities to consider. By weaning ourselves off of the TIF system, we’re freeing an additional portion of Chicago’s property tax base to draw from. For the city, this is offset by the additional spending in the form of this bond, but the city isn’t the only taxing entity to that tax base. I’m thinking in particular about Chicago Public Schools, which we haven’t talked too much about yet but is facing some enormous fiscal gaps in coming years. Expanding their tax base strikes me as a positive to their fiscal position.

For what it’s worth, I’m not alone in that opinion. Moody’s, the major bond ratings agency, released a note in late April covering the plan. Their report highlights several credit positives to the shift, including more predictability for city revenue (via the increased property tax base replacing our reliance on TIF surplus funds), better transparency and budget management by having these dollars flow through the budget process instead of the TIF expenditure process, and more spending flexibility by the city to invest where development dollars are most needed. The key conclusion is that the incremental debt service incurred by the bond issuance seems quite reasonable compared either to the incremental tax base the city picks up by letting TIF districts expire or to the other budgetary benefits the plan involves. The Civic Federation has also expressed support for the plan, with President Joe Ferguson testifying in favor of the plan as a “sensible means of re-setting the City’s over-usage of TIF funding while redirecting revenue to the City to back these bonds for years to come without increasing taxes.”

The key point here: this isn’t just some giant tax-and-spend scheme that’s wasting public resources. It’s a very sensible proposal which moves us away from a crappy funding mechanism (TIFs) towards a better one (the city’s budget) which happens to involve an incremental debt raise along the way.

A look at the spending in particular

I do think it’s worth diving into exactly where these funds are going, to get a sense for what kinds of programs the city is planning on emphasizing going forward. From the city’s website, here’s a breakdown of how those funds will be allocated those funds will go:

By my math, about 75-80% of the total spending here goes towards funding modified or expanded versions of existing programs, rather than brand new things. That strikes me as a good thing. It’s consistent with the idea that we’re primarily looking at a shift from TIF-financed development to bond-financed development, with some spending changes, rather than a gigantic new unproven spending venture.

Getting a bit more specific, the city’s bond book also notes that over the last four years, DOH and DPD have received around $300 million annually from TIF funds, with a 63%-37% split between the two. I mention that because I think it’s noteworthy the new plan is a 50%-50% split between the two departments, skewing things a bit more in favor of the development side than what we’ve had before - that strikes me as a good idea if encouraging growth is our ultimate goal here. The book goes into more detail on these programs beginning on page 13.

On the development side, the main focus (about 70% of spending) is on expanding the Community Development Grants (CDG) program, which funds non-residential real estate projects (both rehab and new construction), with an emphasis on disinvested neighborhoods that need revitalization. So long as it’s done with proper oversight, this seems straightforwardly good to me, and I like the idea that we’re expanding an existing program rather than spinning up some brand new thing.

The next largest chunk - about $100 million - is intended to create a revolving loan fund for the city to make small and medium business loans. On the face of it, this again seems like a good idea to me. I like the fact that it’s a loan program, with the city getting repaid on its investments rather than just giving money away to try and foster growth. That also means our dollars can go further (the “revolving” component), with the repayments going towards subsequent rounds of lending to other businesses.

The third largest portion of development spending seems is $50-75 million set towards a housing infill strategy - redeveloping vacant lots into housing in areas where development has been slow. This was one of the areas highlighted by Urban Environmentalists as particularly pro-housing, and a lot of the program specifics are oriented around reducing barriers to construction (like coming up with pre-approved designs for construction, and taking care of the infrastructure work needed to get lots ready for development). It seems like a good way for the city to support new housing development at scale and reduce cost to develop.

On the housing side, the largest chunk ($250 million, or 40%) is set towards increasing the production of affordable rental homes. This is specifically outlined as something that relies on a lot of TIF funds today - but relying on the bond instead of TIF funds will allow additional flexibility for these affordable housing projects to be developed in neighborhoods not specifically within TIF districts today. I am not an expert on what DOH does, but this seems like what I would assume their bread-and-butter type projects are - building affordable housing. Another 20% or so (around $125 million) is indexed towards what they call a Green Social Housing Revolving Fund, which would seed a low-cost construction lending fund for projects where the developer is committed to selling the property back to the city when completed. I’m not able to find much information on the ‘Green’ part of the fund, but the overall concept is modeled on a similar fund in Montgomery County, Maryland, which is able to reduce the cost of capital for developers and make affordable development more feasible. Again, I like the idea of revolving funds - and this section of the city’s documents has a lot of emphasis about how this chunk of spending is particularly subject to City Council oversight and approval, given that the program will require a new ordinance be passed by the Council to move forward. If we can do it right, this seems like a positive way for the city to increase our housing supply.

There’s then another 20% or so ($125-145 million) towards down payment assistance and homeowner support which makes up my least favorite spending program. As my friend and housing supply advocate Luca Gattoni-Celli5 outlined recently in Newsweek, increasing subsidies to help buyers purchase homes isn’t enough to make housing more affordable at a broader scale, particularly given the reality that if subsidies lead to increased demand for housing, they also have the potential to increase prices. I’m pretty skeptical that a program providing grants of up to $100,000 to help people make down payments is the best use of our housing dollars - I’d rather see us go further to expand other supply side measures, whether that’s building even more affordable rental homes, expanding the DPD’s CDG program further, or something else. Demand-side subsidies just don’t seem optimal.

Another 15% or so goes towards two preservation programs (both expansions of existing programs), working to (1) revitalize troubled, vacant or abandoned housing and (2) preserving our supply of Single Room Occupancy (SRO) buildings. Both of these seem great. For one, the ROI on households/units of housing impacted per dollar spent seems really good here (under $100,000 per household/home supported), which makes sense given that we’re fixing up something that exists rather than creating something new. It also stands to have some spillover effects (as Block Club Chicago outlined last year, decaying vacant homes have contributed towards a whole slew of other neighborhood problems, like rats, drugs, and gunfire, and fixing them up would probably help a lot with that). Finally, I like the acknowledgement that SROs have a role to play in solving our housing shortage in Chicago. I think many people often think of SROs as a crappy form of housing and something we should get rid of, while forgetting that the alternative is not usually ‘some better form of housing’ but is instead ‘no housing at all.’ Preserving SROs seems like an acknowledgement that any housing is better than none, which I think is a good thing.

Some things I have hesitations about

Now, all of the above being said, I do want to make it clear that I don’t necessarily think this is a perfect plan which I have no concerns with.

For starters, we are talking about a lot of money here - and a repayment plan that’ll last for a few decades. I thought Alderman Bill Conway’s proposal to start with a smaller pilot program ($750 million over the next three years instead of $1.25 billion over the next five) was a pretty reasonable one - particularly since it wouldn’t have reduced the per-year spending. Sticking with Conway6, I also wish his proposal to lower the threshold for for individual projects to require City Council approval were given more credence - if one of the worst parts of the TIF system was the lack of oversight, I think making sure we have sufficient oversight on this go around is a good idea (though I do still think the $5 million threshold is reasonable and an big improvement).

Finally, as in all things I always come back to pensions and the budget. In the past few years, our budgets have increasingly relied on TIF surplus revenues to close the budget gap - and those gaps are only expected to grow. I had been hoping that as those TIF districts roll off, at least a portion of the incremental tax base the city was picking up would go directly towards bridging those gaps - and continuing or increasing our supplemental pension payments the city’s been making. I’m at least a little bit concerned about how viable that is going forward in the near term - a concern that seems shared by at least one Alderman, Andre Vasquez (from WBEZ):

Vasquez said he wants to see a portion of the funds dedicated to contributing to the city’s underfunded pensions.

“We don’t want to get to the point where we’re just borrowing money and just spending as opposed to paying off some of the debt and the pension debt, which has been weighing us down,” Vasquez said.7

I think that’s exactly right - which is partially why I think it’s interesting that both Moody’s and the Civic Federation view the bond as a net positive. Again, I think the key is not whether the plan is perfect - it’s about whether it’s a net positive relative to our current baseline of TIF reliance, and by that standard I think it’s certainly a win.

The Bottom Line

The development bond is a big deal.

$1.25 billion is a lot of money - but our TIF property tax base is huge, and big enough to pay for it. Spending on economic development growth is also different than spending on something specious or wasteful.

TIFs are a flawed, inflexible and imperfect tool, and it’s good that we’re getting away from them. Compared to our current approach for development, this is a positive step which moves us in the right direction.

Restating from last time: I think this means our property taxes are roughly 19% higher than they otherwise would be in the absence of any TIF districts, because we’re raising the same amount of tax revenue from a tax base which is 16% smaller (back of the envelope math: 1.00 / 0.84 = 1.19), but I’m only pretty sure that that’s the math I’m supposed to do. Please feel free to write in with a correction if that’s wrong.

The Kinzie Industrial Conservation Area TIF district

That can also be - and often is - extended as well

They reference recent city GO bond issuances to fund housing development in Austin, Charlotte, Denver, Los Angeles, Miami, and New York City, among others - see Appendix I beginning on page 34.

I’d encourage anyone who cares about housing outside of a Chicago-specific context to check out his excellent Substack as well.

For the record, Conway did not vote in favor of the final bill.

For the record, Vasquez did vote in favor of the final bill.

Great article Conor! Considering we’re at the all time high for Chicago households and how intense the rent increases have been as late, I really hope between this and the Cut the Tape initiative we get some much needed housing supply. A lot of commentators question the need for affordable housing in Chicago, but even the cheaper neighborhoods have a dearth of family sized units. Keeping those families here in Chicago is particularly important for CPS as well. Are you thinking of doing an analysis of Cut the Tape? I’d love to see your thoughts.

I'd be very curious to see the differential growth rates of TIF neighborhoods vs. non-TIF neighborhoods, controlling for obvious things like their initial level of wealth, crime rates, etc. Hopefully this has been studied.